In this month’s WWW we reflect on some historical events to contextualise how the political cycle has changed the direction of capital requirements for US banks and what it means for fixed income investors.

The 16th of March 2026 marked the 18-year anniversary of the Federal Reserve rolling out the emergency ‘Maiden Lane’ facilities to back stop JPMorgan’s purchase of Bear Stearns. The event ended 85 years of Bear’s independence having survived the great depression (a mere five years after its founding), WWII, the savings and loans crisis and the collapse of LTCM. The personal habits of the CEO for the 15 years leading up to its failure, James Cayne, a former taxi driver and scrap metals salesman, reportedly included late starts, lots of golf, competitive bridge tournaments, cigars1 and ironically monitoring single name credit default swap levels.

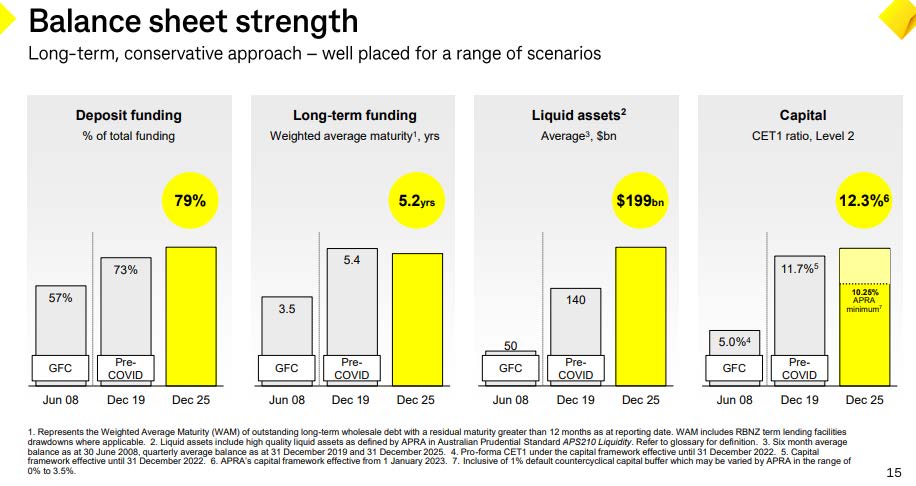

While neither Bear nor Lehman were banks and the Fed even generated a $2.5bn profit on the initial Maiden Lane facility2, the GFC was the catalyst for a globally coordinated material strengthening in bank regulation. In some respects, the tailwinds of more capital, more liquidity and stronger funding, has made this era a relatively easy time to be a top-down fixed income investor in the banking sector. Banks have not been shy in reminding analysts of the changes. The slide decks of most bank funding teams have typically included something similar to the example from CBA below to show the progression of key metrics vs the pre GFC era:

The danger of a top down only approach to banks has of course been punctuated by stress in European banks during the 2010-2012 sovereign crisis and more recently by the failure of Silicon Valley Bank and Credit Suisse. The later episodes were reminders that banking remains a business of maturity transformation with a still healthy dose of leverage. The business model of borrowing short and lending long has always been and remains a bit of a confidence trick. Strong brands and capital metrics are undoubtedly better than the alternative but can ultimately still mean little in the event of enough depositors wanting their money back all at the same time. The expanded access that many banks enjoy to central bank liquidity facilities alongside retail deposit insurance (and the exogenous support provided during the COVID period) is arguably an implicit admission of such ongoing inherent vulnerability.

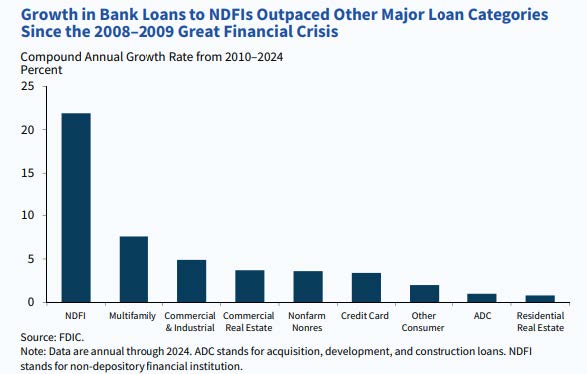

Stronger capital, liquidity and funding profiles did however not come without a cost to return on equity (albeit even equity investors appear to appreciate stronger metrics in deriving valuations). The RoE pressure and more micro aspects of regulation (such as the 6x leverage guidance cap for US LBOs that ran from 2013 to 2017) in turn prompted a change in the mix of bank lending and opened the door neatly for the private credit boom. For US banks specifically, this became apparent in the form of lending to Non-Deposit Financial Institutions (NDFIs) growing at post GFC compound annual rate of 22%, massively outstripping the next strongest loan category of multifamily real estate with a CAGR of just 8%.

The Federal Deposit Insurance Corp (FDIC) defines NDFIs as entities and structures including private equity funds, mortgage lenders, private credit funds, insurers, Real Estate Investment Trusts, Business Development Companies, securitization vehicles, and other special purpose entities. The FDIC further notes that the growth in lending to NDFI’s has been concentrated in large banks and this in turn is focused on loans to private equity and private credit entities. The good news is this is not as scary as might notionally sound. The FDIC further notes in its 2025 risk review ‘’ The composition and structure of bank loans to NDFIs generally exhibit a lower degree of credit risk. Most of the credit facilities to NDFIs are short-term revolving credit lines that are typically collateralized with conservative advance rates against the collateral pledged, providing a layer of loss protection. Supervisory observations reflect strong historical performance and more favourable credit ratings for banks’ loans to NDFIs compared to traditional commercial loans.’’

To the extent that lending to NDFIs is now effectively providing a degree of incremental credit enhancement to large banks from topical sectors such as commercial real estate and software would very likely please the original proponents of the post GFC reforms. The bad news is FDIC 2026 risk review on lending to NDFI’s will likely have to acknowledge the risks including fraud that have been highlighted by collapse of Tricolour and MFS.

As recently as September 2024, US bank regulators were still pushing for higher capital ratios, albeit toned down materially from 2023 proposals that called for an incremental 16% rise in CET1 requirements3. This push however effectively ended with the ‘resignation’ of Michael Barr from the position of vice chair of supervision at the Fed in February 2025. Trump’s nomination of Michelle Bowman to the position in March 2025 became effective in June 2025 and has materially changed the regulatory environment for US banks. Bowman has described the post GFC reforms as initially necessary but ‘’… overly calibrated requirements on low-risk activities produce unintended consequences. Many of these requirements have constrained credit availability, pushed activity into the less-regulated non-bank sector, and added complexity and costs without meaningfully enhancing safety and soundness’’.

Under Bowman, reform of bank leverage ratio rules were completed in December 2025 and come into effect this month4. The next phase of reform for US banks is focused on reducing GSIB surcharges and the impact of stress test shock assumptions. The Fed guides that CET1 requirements for large banks will reduce by about 480 bps5 under a set of measures announced in March. Irrespective of how unlikely Barr’s 2023 proposals were ever going to be implemented, a ~2000+ bps swing in the headline direction of capital requirements from one vice chair of supervision to the next is massive. The experience confirms even bank regulation is now part of the US political cycle and presents a new variable for investors in longer tenor bank instruments to consider. Notably Barr still holds a Fed Governor board position that runs until 2032 and he has strongly advocated against the latest proposals put forward by Bowman6.

On Goldman Sachs’ numbers, large US banks were operating with ~$155bn of excess CET1 capital at the end of 2025 which will now rise by a further ~$50bn. Equity investors are naturally putting their hands in for some of the excess to be returned via buybacks and dividends, but the regulatory intent seems biased towards ultimately directing more bank lending directly to end customers (especially mortgages and related servicing) and by default, lower lending growth rates to NDFIs. That these changes coincide with the first meaningful cyclical challenges within the private credit industry and the growth of NDFIs more broadly, should reinforce the fulfilment of Bowan’s objective for more competitive neutrality.

In Australia, APRA recently announced a consultation that could lower risk weights for banks using the standardised framework7. While a lot more detail is required before being able to objectively assess the proposals, it notionally appears minor in nature and is unlikely to be a precursor to bigger changes. For fixed income investors, picking bank credit will still involve a subjective judgement of a bank’s ability to portray confidence (and an assessment of the CEO’s personal habits for red flags) but one with a need for a more bottom up/name driven approach than the environment afforded by the last 18 years of regulatory tailwinds.

1https://www.vanityfair.com/news/2008/08/bear_stearns200808-2?srsltid=AfmBOorpLN6xNH6Hrud6Uiq3muKj8zDa3w4EURzVrnG5Ujkbhs1ShV

2https://www.newyorkfed.org/newsevents/news/markets/2018/an180918

3https://www.federalreserve.gov/newsevents/pressreleases/bcreg20230727a.htm

https://www.federalregister.gov/documents/2025/12/01/2025-21626/regulatory-capital-rule-modifications-to-the-enhanced-supplementary-leverage-ratio-standards-for-us

5https://www.federalreserve.gov/aboutthefed/boardmeetings/files/board-memo-basel-gsib-standardized-approach-20260319.pdf

6https://www.federalreserve.gov/newsevents/pressreleases/barr-statement-20260319.htm

7https://www.apra.gov.au/news-and-publications/apra-to-consult-on-enhancements-to-bank-capital-and-liquidity-frameworks