The dangers of long COVID

Like most, the memories of COVID seem like a dream. For most of society, lives have moved back to normal with a few exceptions such as the working from home revolution. But some are still suffering the after-effects of COVID and are a shadow of the people they were back in those innocent days of 2019.

We still talk about long COVID, which refers to a bout of COVID where the symptoms persist for longer than 4 weeks, but these days we are talking about companies and not individuals. A company with long COVID is one where earnings are trailing 2019 levels combined with a balance sheet saddled with more debt.

Even if they are still recovering, companies suffering from long COVID may never get back to where they were in 2019. Even if revenues get back to 2019, earnings will be weighed down by higher interest costs and elevated debt levels with balance sheets acutely exposed if a recession does happen in the next few years.

If a recession does indeed eventuate, interest costs will likely increase pushing balance sheet repair further into the future. Long COVID could really be looooooooong COVID.

In our view, credit markets are not sufficiently pricing for long COVID risk. For an investment grade borrower, long COVID may mean that a borrower can never return to the credit risk profile it had in 2019. For a high yield borrower, long COVID may mean that a borrower is wholly reliant on equity to avoid a default.

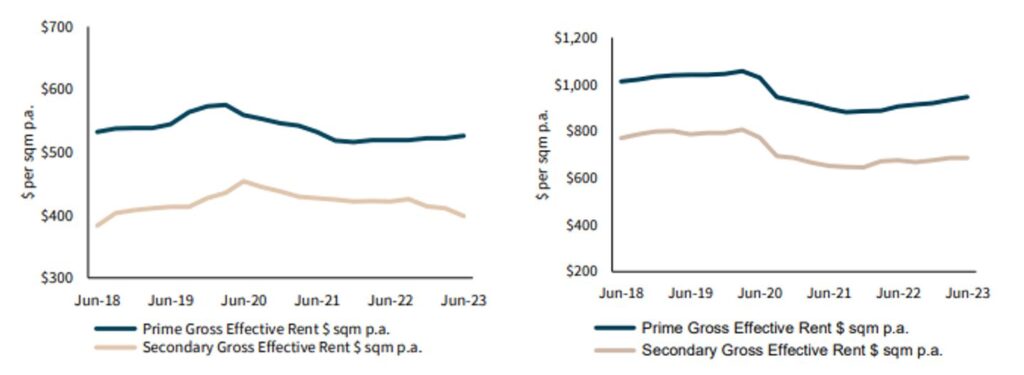

We’ve already written about the office sector of the commercial real estate market. Over the last four years, gross effective yields rents have gone backwards as the same time as debt levels have increased. The rise in interest rates has pushed interest coverage close to one time meaning after interest payments there is little ability to pay down debt to right size the capital structure. The only cure for long COVID is for the asset owner to tip in more equity to pay down debt and right size the capital stack but who has appetite for that when asset values themselves are declining.

Gross Effective Rents Melbourne (LHC) and Sydney (RHC)

Source: JLL Research as at Q2 2023

However long COVID has spread well beyond commercial real estate. Across the ASX300, around 10% of companies have seen earnings decline over the past 4 years and debt increase by 50%. In the United States, 6% of companies have seen earnings decline and debt increase by 50%.

Consider the tourism sector. The post COVID rebound feels immense but then so was the hole that COVID created. A good example of this is Carnival Corporation, one of the largest cruise line operators in the world. COVID was a horror period for them with effectively no revenue for two years but over the past 12 months their customers have returned in droves, seemingly putting COVID in the rear view mirror.

While revenues have recovered, earnings are expected to finish 2023 around 20% below 2019 levels before returning to 2019 levels in 2024. Even at 2019 earnings, free cash flow is only expected to be $1-2 billion per annum implying that without an equity injection it would potentially take up to two decades to get back to 2019 levels of debt.

While that may seem dire, consider that if a recession takes place and earnings flatline at 2023 levels there will be no free cash flow to pay down debt. Indeed in 2023 net debt is expected to increase by over $1 billion.

Despite this outlook, S&P has Carnival B-rated with a positive outlook. Secured debt is rated BB-. S&P sees leverage at around 7 times, improving to 5 times by end of 2024, essentially implying earnings around 15% higher than 2019 levels. The market seems to agree with this sentiment pricing a recent senior secured deal at a spread of 2.85%, broadly flat to the BB high yield index.

While it may seem as though we are trying to second guess the rating agencies and even market pricing of Carnival credit risk, that is not our intention. The key point is that sufferers of long COVID are acutely exposed to the combination of elevated interest rates and the risk of recession. We are still far from 2019 levels of health. If earnings flatline, it is difficult to see how borrowers who are still suffering from long COVID can return to health.